Listen to This Blog Post

Private equity entered 2026 with improving momentum, led by a resurgence in venture capital and a meaningful recovery in deal and exit activity. While fundraising conditions remained challenging, the broader private equity market benefited from renewed investor optimism around artificial intelligence (AI), improving financing conditions, and a more active mergers and acquisitions (M&A) environment.

Details on Year-End Private Equity Activity

Fundraising | Raising capital continued to face headwinds in 2025. Total fundraising fell 22% year over year, while the number of funds closed declined 40%, reflecting continued concentration among the industry’s largest managers. Slower fundraising largely followed the muted dealmaking and exit environment that persisted through much of 2024, which constrained the amount of capital available for new commitments.

The data also highlights the increasingly selective environment facing institutional investors. Larger, established firms continued to capture a disproportionate share of available capital as limited partners prioritized existing relationships and sought to manage constrained private markets pacing budgets. Although fundraising conditions remained difficult through year end, improving transaction activity in 2025 may support a more constructive fundraising backdrop in 2026.

Deal Activity | In contrast to fundraising, deal activity rebounded significantly. Total private equity deal volume climbed 34% year over year in 2025, driven by strength across both buyout and venture/growth equity strategies. Despite the increase in invested capital, deal count declined 13%, underscoring the continued dominance of larger “megadeals.”

Buyouts | Buyout activity strengthened during the second half of the year following a brief slowdown in 2Q25 after “Liberation Day.” Subsequent interest rate cuts helped restore confidence and supported a pickup in larger transactions. Annual buyout deal volume increased 10% year over year, while deal count remained relatively flat. Several high-profile acquisitions—including Walgreens, Electronic Arts, and Endeavor—helped drive the increase in average transaction size.

The stronger transaction environment also pushed valuations higher. Median buyout EV/EBITDA multiples returned to double-digit territory by 4Q25, reflecting improving financing conditions and increased competition for assets.

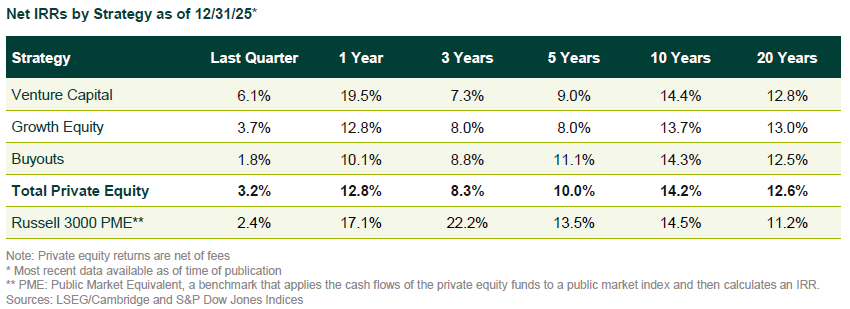

Venture Capital | Venture capital remained the strongest-performing segment of private equity in 2025. The strategy gained 6.1% in 4Q25 and nearly 20% for the full year, benefiting from continued enthusiasm surrounding AI-related companies. Venture capital also generated the strongest long-term performance among the major private equity strategies over the last 10 years.

The current environment increasingly resembles a renewed venture capital “boom” period. Late-stage venture activity accelerated meaningfully as crossover investors re-entered the market and several large late-stage funds returned to fundraising. Venture and growth equity deal volume increased 32% year over year, although activity remained heavily concentrated in a small number of large AI-related financings, including OpenAI and Anthropic.

Exits | After several years of subdued realizations, exit activity rebounded meaningfully in 2025. Total exit volume increased 53% year over year as both M&A and IPO markets reopened. Despite the improvement, exit activity remained below prior-cycle highs at roughly 70% of 2021 levels.

Several notable IPOs reached the market in 2025, including CoreWeave, Klarna, and Circle. Looking ahead, market participants continue to monitor a potentially robust 2026 IPO pipeline that may include companies such as SpaceX, Anthropic, and OpenAI.

Improving exits also provided some relief for limited partners seeking liquidity. Distributions totaled 12% of beginning net asset value (NAV) in 2025, still well below the historical norm of roughly 20%, but importantly marked the first year since 2021 in which distributions exceeded contributions.

Returns | Private equity generated a solid 12.8% return for the year and 14.2% annualized over the last 10 years. While trailing public equity over shorter periods following the sharp rebound in listed markets, private equity continued to compare favorably over longer horizons—particularly relative to small cap public equities.

Dry powder also reached a new record high in 2025, surpassing $3 trillion globally. The continued growth in undeployed capital reflects both the long-term expansion of the asset class and the uneven pace at which capital has been deployed over recent years.

Overall, 2025 marked an important transition year for private equity. Fundraising conditions remained difficult, but improving deal activity, stronger exits, and renewed enthusiasm surrounding AI helped restore momentum across much of the market.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.