Listen to This Blog Post

U.S. stock market concentration has become a topic of frequent discussion by market participants. The S&P 500 may have 500 companies, but the top 10 now make up a historically large share of the index, and much of the market’s return. The Nasdaq-100 is even more concentrated, with its top 10 names making up close to half the index.

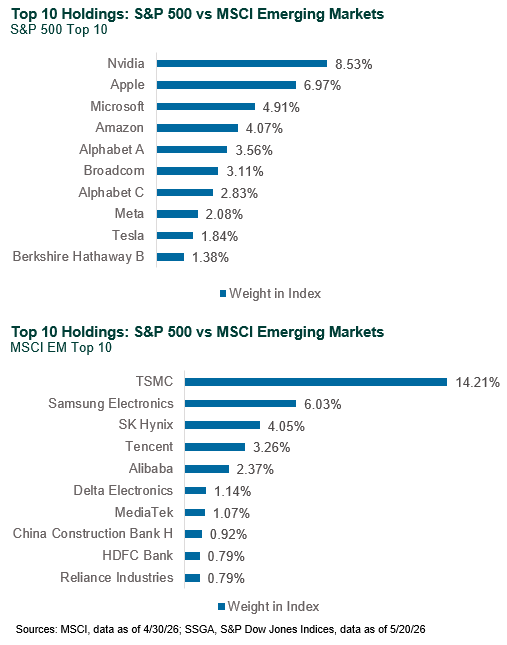

This does not mean these indices are broken. It means market-cap weighting is doing exactly what it is supposed to do. The biggest companies get the biggest weights. The companies that compound the fastest become harder and harder for institutional investors to avoid. But that also means the S&P 500 is not a perfectly balanced representation of corporate America. It is a lot of Nvidia, Apple, Microsoft, Amazon, Alphabet, and friends.

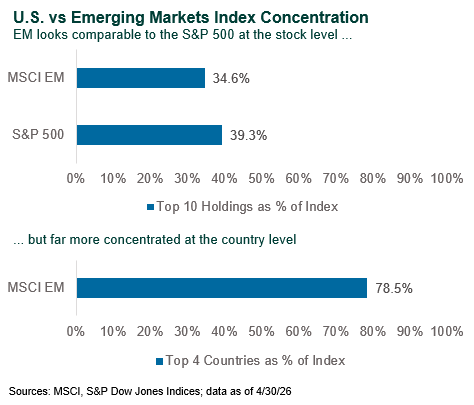

Emerging markets, it turns out, are not that different. Investors often evaluate emerging markets as if they are one big, diversified entity: China, India, Brazil, Mexico, Saudi Arabia, South Africa, Southeast Asia. A little bit of everything. And on paper, that sounds right. The MSCI Emerging Markets Index has more than 1,200 companies across 24 countries. That sounds pretty diversified.

But under the hood, Taiwan is now roughly one-quarter of the index. China is a little less than one-quarter. South Korea is close to one-fifth. India is around 12%. Brazil, once one of the classic emerging market stories, is less than 5%. So, if you put $100 into the MSCI Emerging Markets Index today, roughly $79 goes into just four countries: Taiwan, China, South Korea, and India. That is not exactly “a little bit of everything.”

This concentration did not appear overnight. A decade ago, the MSCI Emerging Markets Index was already somewhat top-heavy, but not nearly to the same degree as today. In 2016-17, the largest MSCI EM constituent was only around 3% to 4% of the index, the top 10 constituents made up roughly 23%, and the four largest country weights—China, South Korea, Taiwan, and India—totaled about 63%. By 2021, the story had become much more China-centric, with China alone approaching 40% of the benchmark. Today, the index is even more concentrated, but its center of gravity has shifted. China remains large, while Taiwan and South Korea have also become significant index weights. So the concentration problem did not just grow; it changed shape.

The company concentration is striking too. TSMC (Taiwan) alone is more than 14% of the index, and a stunning 57% of Taiwan’s total weight in the index. Samsung (South Korea) is around 6%. SK Hynix (South Korea) is around 4%. Put those three companies together and you get almost one-quarter of the entire MSCI Emerging Markets Index. So emerging markets today are not just China, commodities, banks, and cheap manufacturing. They are China, but also increasingly global AI infrastructure, semiconductors, memory, and India. That is not necessarily bad. TSMC, Samsung, and SK Hynix are some of the most important companies in the world. If AI, data centers, advanced chips, and memory are among the biggest investment stories of the moment, then of course they show up in the index.

But it does change what investors actually own. The U.S. concentration story is mostly about AI-related companies. The EM concentration story is about AI-related companies and countries. Investors may think they are getting broad exposure to the developing world. But in practice, they are getting a very large allocation to Taiwan, China, South Korea, and India, with a huge semiconductor engine inside it. That is a double layer of concentration.

This does not mean institutional investors should abandon emerging market exposure. But it does mean investors should know what they own. A passive EM allocation today is not simply broad exposure to the emerging world. It is a concentrated allocation to the largest listed companies in a few emerging markets, especially Taiwan, China, South Korea, and India. When evaluating active emerging market equity managers, investors should not simply be asking whether they have beaten the MSCI Emerging Markets Index over the last three or five years. The more informative questions include how they are dealing with the index’s concentration. Are they intentionally underweight or overweight semiconductors, China, or India? Are their returns coming from stock selection, country allocation, thematic allocation, or factor exposure? Has their style approach been a significant beneficiary of the current AI tailwinds? Was it skill or good fortune a manager was well positioned for the recent rally in all things related to AI? In a concentrated benchmark, a good active EM manager should be able to explain not just what they own, but also what they are choosing not to own and why.

It turns out that concentration has become a defining feature of modern equity indices. In the U.S., that concentration is Nvidia, Apple, Microsoft, Amazon, Alphabet, and friends. In emerging markets, it is TSMC, Samsung, SK Hynix, China, Taiwan, South Korea, and India. Different names. Same math. And the same considerations for institutional investors.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.