Listen to This Blog Post

How Global Markets in 2Q26 Did

Global equities rebounded sharply in 2Q26 as solid economic activity, strong corporate earnings, and optimism around AI outweighed concerns around inflation and monetary policy uncertainty. Technology stocks resumed market leadership as investors continued to reward companies tied to AI and digital infrastructure. Fixed income markets gained in 2Q as income and tightening credit spreads offset higher Treasury yields. Listed real assets delivered less compelling performance in 2Q relative to recent quarters.

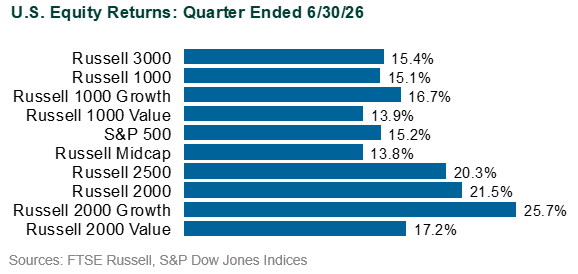

Equities: The MSCI ACWI Index rose 14.9% for the quarter, erasing prior-quarter weakness as risk appetite improved. U.S. equities advanced broadly, with the S&P 500 gaining 15.2% and reaching new highs after recovering from the volatility earlier in the year.

SpaceX’s blockbuster IPO sent shares surging, reaching a $2.7 trillion valuation and making Elon Musk the world’s first trillionaire. The Russell 3000 Technology sector surged 30.0%, significantly outpacing the broader market, while Durables (+14.0%) also benefited from continued capital investment. Energy (-12.3%) was the weakest sector as oil prices reversed sharply from quarter highs and supply concerns eased. Value-oriented and defensive sectors generally lagged the broader market, including Consumer Staples (+4.5%) and Materials (+2.1%). Growth stocks (Russell 3000 Growth: +17.1%) outperformed value (+14.0%), while small caps (Russell 2000: +21.6%) led large caps (Russell 1000: +15.1%) as improved risk sentiment supported more cyclical areas of the market.

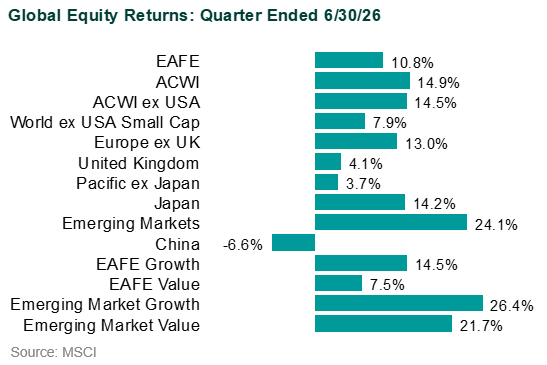

Global ex-U.S. equities also posted strong gains (MSCI ACWI ex-USA: +14.5%) despite a modest rebound in the U.S. dollar (DXY: +1.2%). Developed market equities advanced, led by strength in technology-related sectors and improving investor sentiment. Companies within the euro zone (+15.3%) and Japan (+14.2%) delivered strong returns. Emerging markets were among the strongest performers (MSCI EM: +24.1%), driven by significant gains in semiconductor-linked markets including Korea and Taiwan. Chinese equities were mixed amid ongoing policy support and improving sentiment toward domestic technology companies.

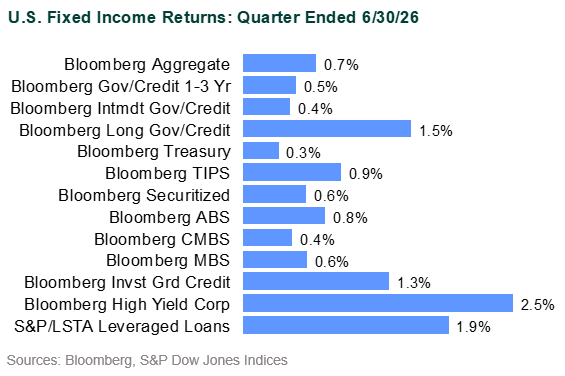

Fixed Income: The Bloomberg US Aggregate Bond Index rose 0.7% for the quarter. Treasury yields increased, with the 2-year rising 35 bps to 4.14% and the 10-year increasing 14 bps to 4.44%. The yield curve flattened as markets repriced expectations for Federal Reserve policy amid persistent inflation concerns. Credit markets outperformed as risk appetite improved and spreads tightened. Investment grade corporate bonds gained 1.4%, while high yield corporates advanced 2.5%, led by lower-rated issuers. Securitized assets posted modest gains, with ABS (+0.8%), MBS (+0.6%), and CMBS (+0.4%) all rising. Municipal bonds recovered after a challenging start to the year, with the Bloomberg Municipal Index up 2.5% and high yield municipals gaining 3.4%. Demand improved during the quarter as yields supported investor flows.

Global fixed income also posted positive results. The Bloomberg Global Aggregate Index gained 1.3% on a USD-hedged basis and 0.9% unhedged, as regional yield movements diverged. Japanese government bond yields continued to rise alongside further monetary policy normalization, while European yields declined. Emerging market debt outperformed developed markets, with hard-currency (JPM EMBI: +4.6%) and local-currency (JPM GBI-EM: +3.9%) indices benefiting from improved investor sentiment.

Listed Real Assets: Commodity markets reversed sharply (Bloomberg Commodity Total Return: -8.1%) following the prior quarter’s energy-driven rally. Although energy was the focal point of the quarter, precious metals also experienced a sharp decline (S&P GSCI Precious Metals Total Return: -14.3%). Meanwhile, natural resources equities also fell (S&P Global Natural Resources Equities: -8.5%) as energy prices retreated from elevated levels following easing concerns around supply disruptions. Interest-rate sensitive real assets performed better despite higher Treasury yields. REITs rebounded strongly (FTSE Nareit Equity Index: +12.4%) as investors returned to the sector following prior underperformance and valuations became more attractive. Listed infrastructure declined slightly (-0.5%), while MLPs generated modest gains (+1.4%).

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.