You are currently viewing this website using the Internet Explorer (IE) web browser. This website has limited functionality in IE, and you won’t be able to download research documents. For an optimal experience, please access this website using any other supported web browser.

Large public defined benefit (DB) plans have found it very difficult to keep investment risk from rising without sacrificing expected returns. Some plans have maintained relatively higher levels of expected return, but may find their portfolios are relatively less diversified and less liquid than peers.

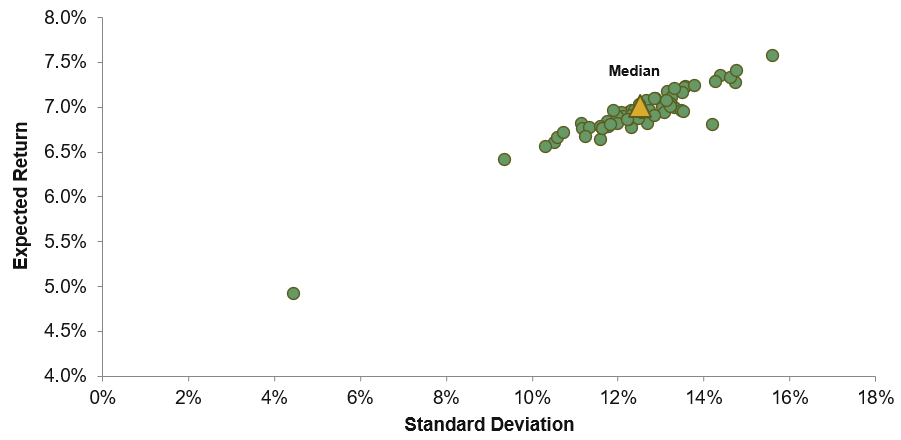

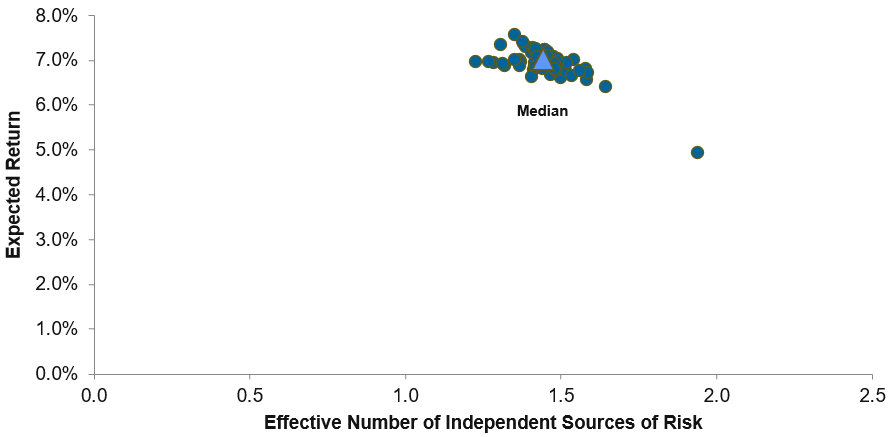

Institutional investors are of course well aware of the tradeoff that higher expected returns come with higher risk. This is evident across a peer group of large public DB plans (>$1 billion) compiled by Callan and analyzed with Callan’s 10-Year Capital Markets Assumptions. (In this and subsequent charts, the median plan is defined as the plan exhibiting approximately the median expected return and median standard deviation within the peer group.)

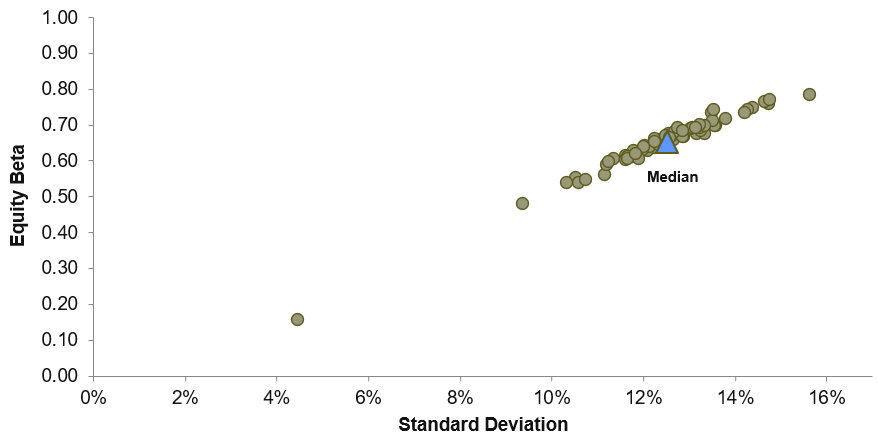

How do public plans take additional risk in pursuit of those higher returns? This is associated with adding Equity Beta into the portfolio. Equity Beta is a useful metric because it captures direct equity exposure, as well as “hidden” or indirect exposure that could be embedded in other asset classes.

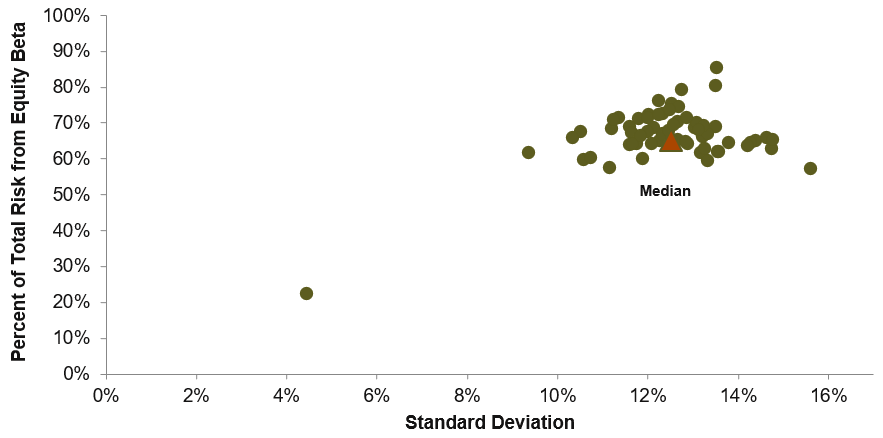

Consequently, public plans typically have about two-thirds of all their risk attributable to Equity Beta, a single factor.

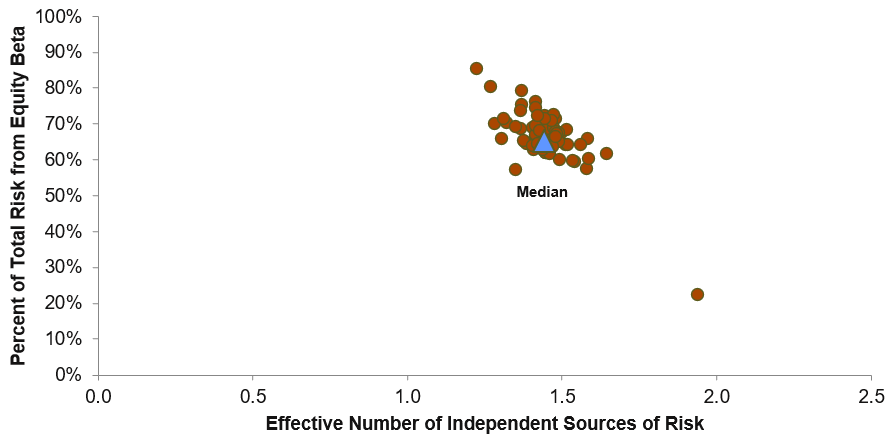

And this is associated with reduced levels of diversification. The level of diversification is quantified using Callan’s 10-Year Capital Markets Assumptions with a metric called the effective number of independent sources of risk.

While many public plans turn to alternative asset classes to simultaneously bolster both expected return and diversification, it’s necessary to be aware of potential illiquidity. Public plans pushing for higher expected returns without increased levels of illiquidity may see reduced diversification levels. Other plans have pursued meaningfully higher expected returns by increasing allocations to illiquid alternatives, primarily private equity, which has the highest expected return of any asset class.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.

For Investment Managers & Advisers

You are now leaving Callan LLC’s website and going to Callan Family Office’s website. Callan Family Office is not affiliated with Callan LLC. Callan LLC has licensed the Callan® trademark to Callan Family Office for use in providing investment advisory services to ultra-high net worth clients, family foundations, and endowments. Callan Family Office and Callan LLC are independent, unaffiliated investment advisory firms separately registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940.

Callan LLC is not responsible for the services and content on Callan Family Office’s website. Inclusion of this link does not constitute or imply an endorsement, sponsorship, or recommendation by Callan LLC of their website, or its contents, and Callan LLC is not responsible or liable for your use of it. When visiting their website, you are subject to Callan Family Office’s terms of use and privacy policies.