Listen to This Blog Post

The global repurchase agreement (repo) market is one of the most systemically important segments of modern financial infrastructure. The repo market is a massive short-term lending exchange in which institutional investors trade trillions of dollars daily to manage cash liquidity and finance securities portfolios. It functions as the central plumbing of the global financial system, allowing institutions to borrow cash by providing high-quality securities as collateral.

At its core, a repo is a short-term borrowing mechanism in which one party sells securities to another with a simultaneous agreement to repurchase them at a specified price on a future date. The difference between the sale price and the repurchase price represents the cost of borrowing—effectively an interest rate known as the repo rate.

The global repo market transacts in excess of $10 trillion in daily volume, serving as the primary mechanism through which banks, asset managers, central banks, and governments manage short-term liquidity, fund securities inventories (securities finance and securities lending), and implement monetary policy. Repo underpins the smooth functioning of sovereign bond markets, money markets, and the broader financial system.

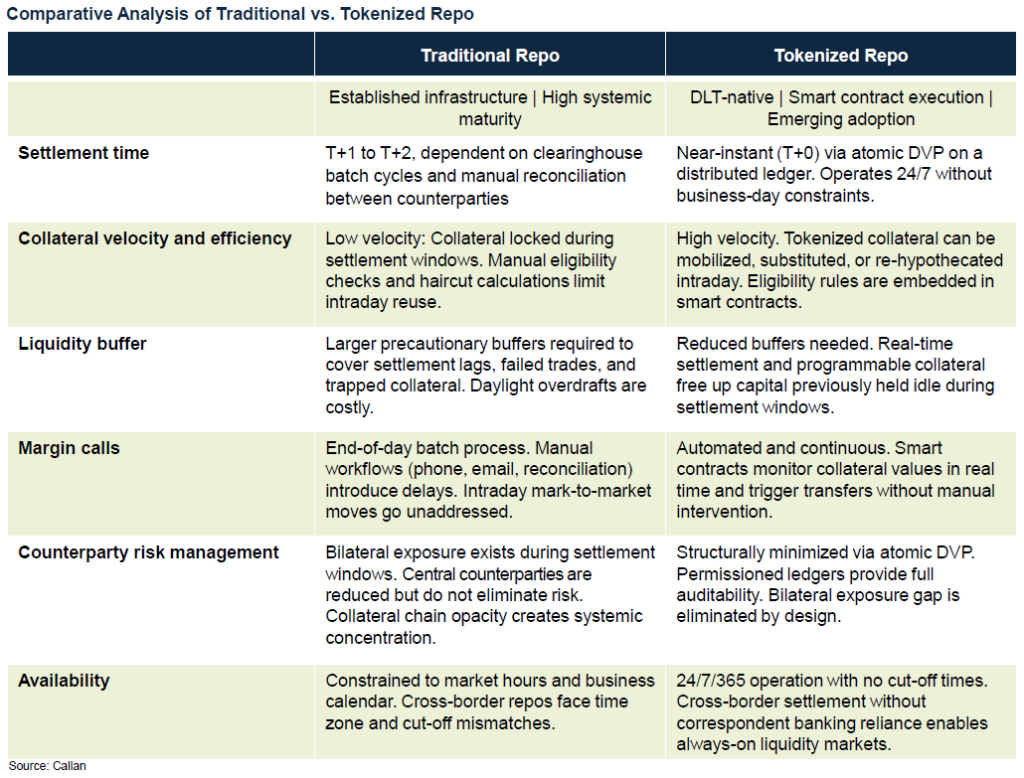

Despite its scale and systemic importance, the operational architecture underpinning traditional repo has changed little in decades. Settlement remains largely a T+1 or T+2 process, margin calls are processed in end-of-day batches, and collateral management relies on a fragmented network of custodians, central counterparties, and correspondent banks operating across different time zones and regulatory jurisdictions.

Introduction of Tokenized Repo

The emergence of distributed ledger technology (DLT) and asset tokenization has introduced a fundamentally different operating model—tokenized repo. By representing securities as digital tokens on a shared ledger and encoding transaction logic in smart contracts, tokenized repo promises near-instantaneous settlement, continuous collateral mobility, automated margin management, and 24/7 market availability.

Neither model can be ignored. Traditional repo remains the backbone of global liquidity management, deeply embedded in regulatory frameworks, legal conventions, and institutional workflows that have been stress-tested through multiple market crises. Tokenized repo, meanwhile, represents a structural evolution that addresses longstanding frictions at a foundational level and not through incremental process improvements, by redesigning the settlement and collateral layer itself. As regulatory frameworks evolve and institutional adoption accelerates, the two models are likely to coexist and converge, making an understanding of their respective characteristics essential for market participants, policymakers, and technology architects alike.

Key Structural Observations

Four cross-cutting themes emerge from comparing the two models:

- Timing is the root issue. Nearly every operational advantage of tokenized repo flows from a single shift: moving from batch, end-of-day processing to continuous, real-time execution. Settlement, margin, and collateral reuse all improve as a downstream consequence.

- Collateral efficiency is the most commercially significant factor. In traditional repo, collateral is immobilized during settlement windows and substitution is laborious. Tokenized infrastructure enables the same collateral to be mobilized multiple times intraday, materially changing balance sheet economics.

- Counterparty risk is minimized because payment and delivery occur simultaneously. This means neither side has to rely on the other to complete its part of the transaction after the fact. As a result, settlement risk is substantially reduced compared with traditional market structures, which typically depend on clearinghouses and collateral arrangements to manage these exposures.

- The primary friction in tokenized repo is legal, not technical. Questions around enforceability of smart contracts, the legal status of tokenized securities under collateral law, and cross-ledger interoperability remain active constraints on adoption—not the underlying technology itself.

Outlook

The evolution of repo infrastructure is not a binary replacement of the old by the new. Traditional repo will remain dominant for the foreseeable future, supported by decades of legal precedent, regulatory recognition, and institutional inertia. However, the structural advantages of tokenized repo are sufficiently compelling—particularly around collateral efficiency, margin automation, and counterparty risk reduction—that adoption will accelerate as legal and interoperability barriers are resolved.

Market participants that understand both models will be best positioned to navigate the transitional period and to develop hybrid strategies that leverage the stability of traditional infrastructure alongside the efficiency gains of tokenized execution. The repo market is not on the cusp of disruption; it is in the early stages of a foundational upgrade.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.