In 2016, Callan published “Risky Business,” a paper that focused on the challenges faced by institutional investors in the low return environment they found themselves in. The paper received a lot of attention, including from The Wall Street Journal, largely due to the graphic illustrating what was required in terms of asset allocation to earn a 7.5% expected return over various time periods. Our analysis found that investors in 2015 needed to take on three times as much risk as they did 20 years before to earn the same return.

Given that attention and the interest in our work from the institutional investing community, we wanted to update our analysis again to reflect current conditions and to extend the comparison over a longer time period.

Our 2024 Capital Markets Assumptions once again rose from the prior year, particularly for fixed income. Our core U.S. fixed income assumption increased 100 basis points to 5.25% for the next 10 years on the back of higher starting yields. We increased our return expectations for public market equity segments by approximately 25 bps from a year earlier, centered around 7.5% for large cap U.S. equity. Returns for private market asset classes rose incrementally. Finally, we maintained our 10-year inflation assumption at 2.5%.

Risky Business 2024: Our Methodology

The impact of elevated interest rates and inflation on housing and the financial markets coupled with threats to the world economy from geopolitical strife leave institutional investors facing a challenging investing environment despite improved return expectations.

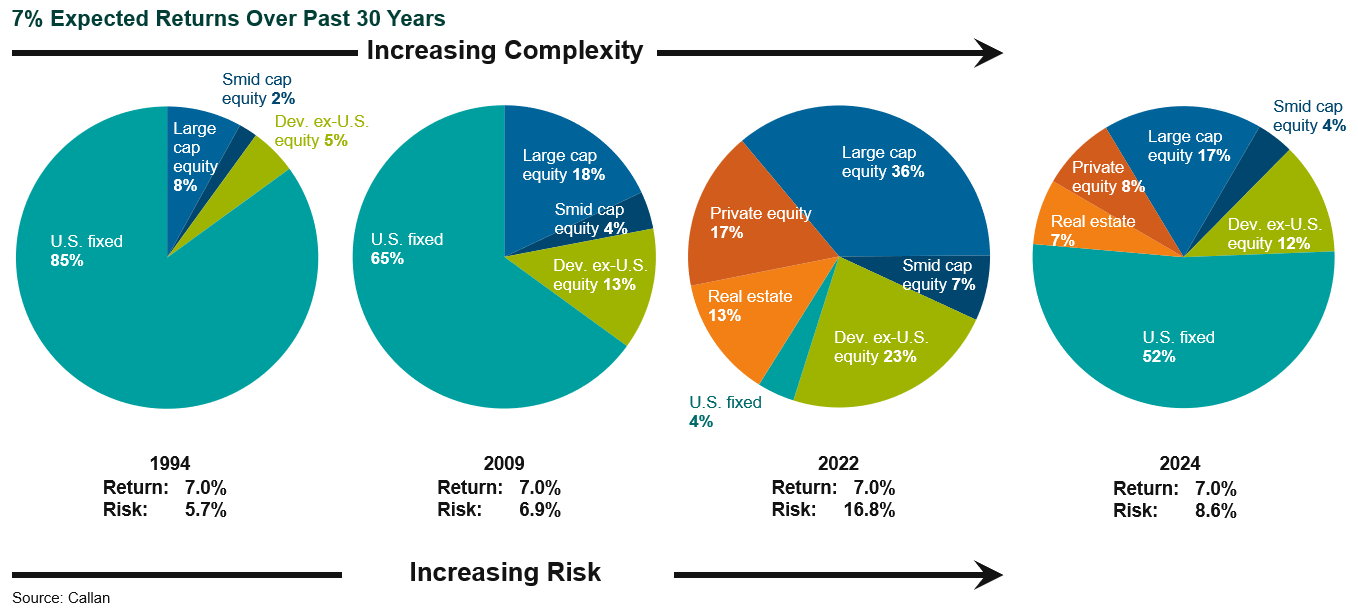

To find out how challenging, our experts examined what it would take for an investor to achieve a nominal 7% expected return over the next 10 years. Using our proprietary Capital Markets Assumptions, we found that investors in 2024 needed to take on 1.5x as much risk as they did 30 years ago, with an additional 33% of the portfolio in return-seeking assets.

Investor portfolios are now more complex than ever. Whereas in 1994 a portfolio made up of 85% bonds and 15% public equity was projected to return 7%, by 2024 an investor would need to include almost half of the portfolio in return-seeking assets (stocks and private markets) to achieve comparable return expectations. Today’s 7% portfolio is much more reasonable than it was just two years ago, though. In 2022 an investor was required to include 96% of the portfolio in return-seeking assets to earn a 7% expected return, while today over half of the portfolio can be in fixed income.

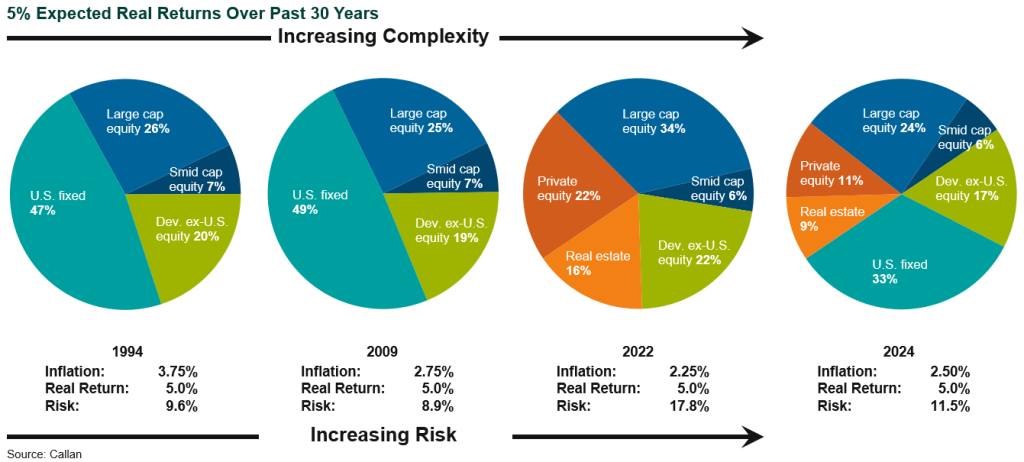

To be sure, the early ‘90s were a different time, with not only higher fixed income yields but also higher inflation. Therefore, we examined what it would take to earn a 5% real return given our prevailing inflation expectations at the time. The graphic below shows that the pattern of increasing complexity over time remains similar over the 30-year period. Today investors need to take on roughly 20% greater volatility than they did 30 years ago to earn a 5% real expected return despite a 125 basis point decline in inflation.

While investors are cautiously optimistic that inflation is coming under control and a recession will be averted, uncertainty surrounding what lies ahead and the impact on portfolios is always on the minds of investors. Whether assessed in a nominal or real framework, our conclusions from our 2016 study remain unchanged: Investors require more complex and risky portfolios to meet their return targets than they did 30 years ago.

While 2024 marks a significant improvement over just two years ago in terms of the risk required to earn a specific return target, clients must continue to assess whether their portfolio’s risk and complexity is appropriate based on their specific circumstances.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.