1Q22 Private Credit Trends

As credit spreads have compressed, institutional investors have pushed into private credit in search of yield, with a balanced private credit allocation to a mix of top quartile to median performers offering a levered return in the 8% to 10% range.

- Yield and income-generating characteristics remain attractive in a low-rate environment.

- Alpha generation can be magnified through strategies that extract a complexity premium.

- Many direct lending assets are floating rate, which can add protection against rising rates.

- Portfolios were resilient during the COVID dislocation due to liquidity injected into the economy; valuations are back to 2019 levels but the space remains crowded.

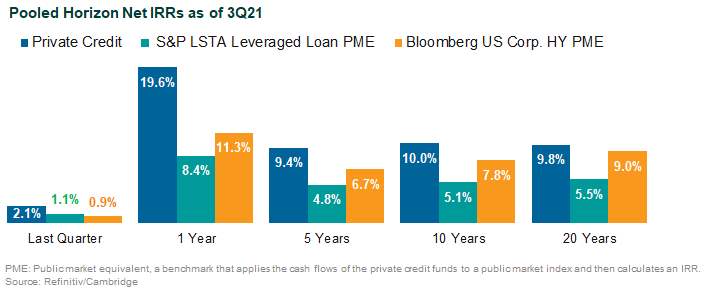

- Private credit performance varies across sub-asset class and underlying return drivers. On average, the asset class has generated net IRRs of 8% to 10% for longer-term trailing periods ended Sep. 30, 2021. Higher-risk strategies performed better than lower-risk strategies.