Listen to This Blog Post

How Global Markets in 1Q26 Performed

Global equities declined in 1Q26 as rising interest rates and elevated macro uncertainty weighed on risk sentiment, with U.S. equities underperforming non-U.S. markets. Fixed income markets were broadly flat to modestly negative in 1Q26, as rising yields and spread widening offset income. Liquid alternatives delivered strong returns in 1Q26, led by commodities and energy-related assets.

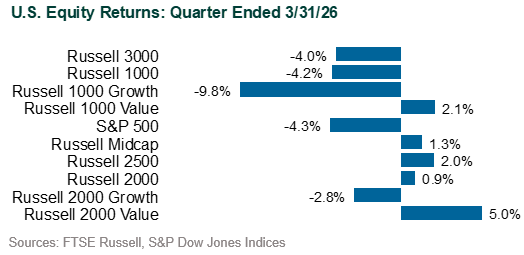

Equities: The MSCI ACWI Index fell 3.2% for the quarter, while the S&P 500 declined 4.4%, driven by weakness in growth-oriented sectors as higher yields pressured valuations. Technology declined (Russell 3000 Technology: -9.6%), with the Magnificent 7 underperforming the broader market as investors rotated away from mega-cap technology stocks.

Energy (+37.0%) was the strongest-performing sector, supported by higher commodity prices and geopolitical tensions, while Materials (+13.8%) and Utilities (+11.5%) also advanced. In contrast, Financials (-7.8%) and Health Care (-4.9%) lagged alongside broader risk assets. Value significantly outperformed growth, with the Russell 1000 Value Index rising 2.1% compared to a 9.8% decline in the Russell 1000 Growth Index, reflecting a rotation toward more defensive and inflation-sensitive segments of the market. Small-cap performance was mixed, with the Russell 2000 posting a modest gain (+0.9%) as value (+5.0%) offset weakness in small-cap growth.

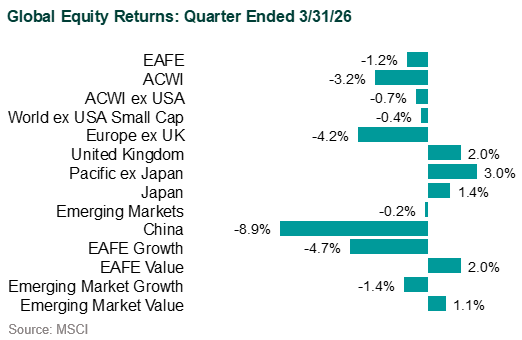

Global ex-U.S. equities were more resilient, despite a modest strengthening of the U.S. dollar (DXY: +1.7%). The MSCI ACWI ex-USA Index declined 0.7%, supported by stronger performance in commodity-sensitive markets and value-oriented sectors. Developed market equities were mixed, with the euro zone down 5.0%, while the U.K. (+2.0%) and Japan (+1.4%) posted gains. Emerging markets were broadly flat (MSCI EM: -0.2%), though performance diverged significantly across regions. Latin America outperformed, led by Brazil (+19.1%), supported by currency strength and commodity exposure, while Emerging Asia lagged, driven by declines in China (-8.9%) and India (-18.1%). Semiconductor-oriented markets such as South Korea (+16.5%) and Taiwan (+9.1%) were notable exceptions.

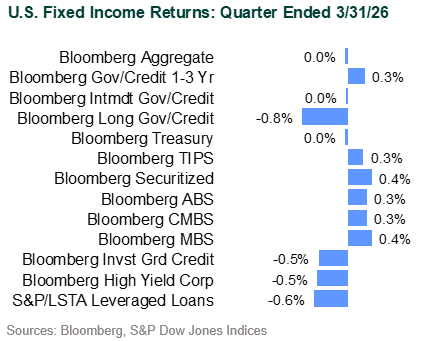

Fixed Income: The Bloomberg US Aggregate Bond Index declined 0.1% for the quarter. Treasury yields moved higher across the curve, with the 2-year rising 32 basis points to 3.79% and the 10-year increasing 12 basis points to 4.30%. The yield curve flattened, with the 2s/10s spread narrowing by 20 basis points. Inflation expectations rose modestly, with the 5-year breakeven increasing to 2.54%.

Credit markets weakened during the quarter as spreads widened. Investment grade corporate bonds (-0.5%) underperformed Treasuries, while high yield declined 0.5%. Leveraged loans also posted negative returns (-0.6%), reflecting softer demand and spread-widening. Securitized assets were a relative bright spot, with MBS (+0.4%), ABS (+0.3%), and CMBS (+0.3%) generating modest positive returns. Municipal bonds declined slightly (-0.2%), though high yield municipals posted gains (+0.7%). TIPS (+0.3%) outperformed nominal Treasuries, supported by rising inflation expectations.

Global fixed income declined (Bloomberg Global Aggregate: -1.1% unhedged, -0.2% hedged) in 1Q, with developed market bonds under pressure from rising yields across regions, including Japan and Europe. Japan’s 10-year yield rose 29 bps to 2.4%, while Germany’s 10-year yield rose 15 bps to 3.0%. Hedged returns fared slightly better as the U.S. dollar strengthened modestly against a basket of major currencies, including the Japanese yen, British pound and euro; the ICE U.S. Dollar Index rose 1.7% during the quarter. Emerging market debt declined in 1Q with local-currency bonds (JPM GBI-EM: -2.3%) performing worse than hard-currency bonds (JPM EMBI: -1.3%) given the currency impact. Returns were mixed within local markets with Brazilian bonds returning 7.3% and Turkish debt falling 6.7%.

Liquid Alternatives: The Bloomberg Commodity Total Return Index rose 24.4% for the quarter, reflecting gains in energy markets amid geopolitical tensions and supply concerns. Natural resources equities (+19.8%) and MLPs (+16.9%) also performed well, benefiting from higher oil and gas prices. REITs (FTSE Nareit: +4.8%) advanced, supported by stable income despite rising interest rates. Gold spot prices experienced increased volatility during the quarter, including a sharp pullback late in the period, partially retracing gains from earlier in the year.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.