You are currently viewing this website using the Internet Explorer (IE) web browser. This website has limited functionality in IE, and you won’t be able to download research documents. For an optimal experience, please access this website using any other supported web browser.

Listen to This Blog Post

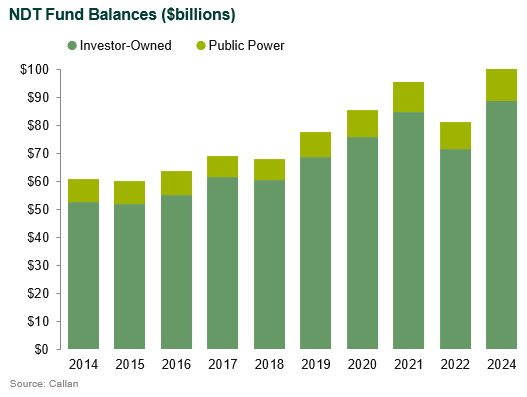

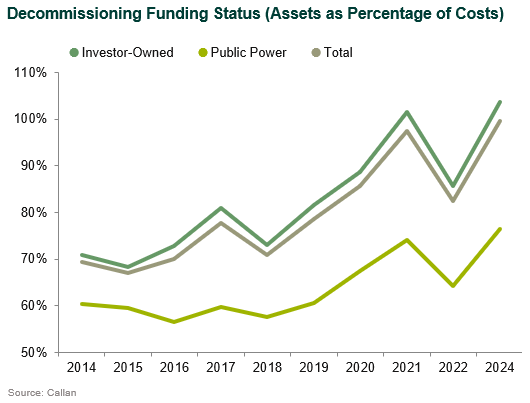

Callan’s 2025 Nuclear Decommissioning Funding Study found that NDT balances totaled $100 billion in 2024. Assets rose over 23% from two years earlier, largely due to stock performance, which saw the S&P 500 up 58% in cumulative terms for the two-year period. Those gains helped funding as a percentage of total decommissioning cost estimates, which rose to almost 100% in 2024, the highest level since this study started in 2007 and a significant increase over the 82.5% level in 2022.

Our study, which offers key insights into the status of nuclear decommissioning trusts (NDTs) in the U.S. to make peer comparisons more accurate and relevant, covers 24 investor-owned and 27 public power utilities with an ownership interest in the 94 operating and 14 of the non-operating nuclear reactors in the U.S. NDTs are created to pay for the costs of decommissioning a closed nuclear power plant, which involves safely removing it from service and reducing residual radioactivity to a level that permits release of the property and termination of the operating license.

Our NDT study also found that total decommissioning costs were up slightly in 2024 to just over $100 billion, a $2.2 billion (+2.3%) increase from 2022, as several updated cost figures more than offset ongoing decommissioning at non-operating reactors. Total contributions from utilities into their NDTs fell to $163 million in 2024, a $208 million (56%) decrease from $371 million in 2022.

Disclosures

The Callan Institute (the “Institute”) is, and will be, the sole owner and copyright holder of all material prepared or developed by the Institute. No party has the right to reproduce, revise, resell, disseminate externally, disseminate to any affiliate firms, or post on internal websites any part of any material prepared or developed by the Institute, without the Institute’s permission. Institute clients only have the right to utilize such material internally in their business.

For Investment Managers & Advisers

You are now leaving Callan LLC’s website and going to Callan Family Office’s website. Callan Family Office is not affiliated with Callan LLC. Callan LLC has licensed the Callan® trademark to Callan Family Office for use in providing investment advisory services to ultra-high net worth clients, family foundations, and endowments. Callan Family Office and Callan LLC are independent, unaffiliated investment advisory firms separately registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940.

Callan LLC is not responsible for the services and content on Callan Family Office’s website. Inclusion of this link does not constitute or imply an endorsement, sponsorship, or recommendation by Callan LLC of their website, or its contents, and Callan LLC is not responsible or liable for your use of it. When visiting their website, you are subject to Callan Family Office’s terms of use and privacy policies.